Think about a scenario where you are a consumer visiting a physical boutique. You select the merchandise you want to purchase, proceed to the counter and pay using your credit card. While doing so, it is expected that you implicitly trust the person handling the transaction is not secretly making a copy of your card details on an under-the-counter notebook or displaying your paper receipt in full view.

In the virtual realm, your physical boutique checkout counter is replaced by your online checkout, while the notebook becomes your website server’s underlying database. Information passing across your online store is intangible, hence highly susceptible to any potential exposure.

The Payment Card Industry Data Security Standard, popularly abbreviated as PCI-DSS, is the international technical and operating standard aimed at ensuring that no such information ever falls into the wrong hands. The PCI-DSS provides the minimum security requirements for any enterprise that handles credit cards.

From running a small storefront using open source software, all the way up to managing a multi-national enterprise backend, PCI-DSS becomes important to you as long as a transaction passes through your network. It’s not some optional “nice to have,” but rather a manual for ensuring the safety of your customers and keeping your shop up and running.

1. Why the Acronym? – What PCI-DSS Means

It’s easy for people who run businesses to assume that compliance with PCI-DSS is just another thing you must do because banks force you to do so. But beyond all that red tape, compliance has a lot more to do with building and maintaining trust.

Unshakable Customer Trust

When a consumer clicks onto your website, hesitates for a moment, and inputs their 16 digit credit card number along with other necessary information, they are taking a big risk in terms of trust.

All of it can vanish into thin air after a single data breach. Consumers are not going to punish the hackers in this case; they will put the blame squarely on you—the organization that did not provide proper protection for their sensitive information. By following strict PCI-DSS standards, you demonstrate to your customers, business partners, and stakeholders that you are dedicated to handling personal information responsibly.

How to Avoid Catastrophic Financial Consequences

Non-compliance is a very costly mistake indeed. The fact is, payment brands do not impose fines on merchants themselves, but rather on your acquiring bank, and the latter does it for you.

- Monthly Fines for Non-Compliance: For violating regulations, your acquiring bank may charge up to $100,000 per month, with varying amounts depending on the nature and degree of the infringement.

- The Price Tag of a Security Breach: In the event of a security breach when operating without meeting compliance, the financial consequences become even more drastic. You will incur huge expenses related to conducting forensics analysis, providing credit monitoring for your users, replacing lost cards, etc.

- The Merchant Blacklist: In In the extreme cases of negligence in terms of being out of compliance, the credit card brand could pull all your rights to continue with any kind of processing. Placing you on the merchant blacklist will mean that your business cannot process any credit card, which will essentially shut down your online shop.

The Threat Environment in a v4.0 Era

Cyber threats have become extremely advanced in the past decade. The era of simple database breaches is now long gone. New cybercriminals utilize highly dynamic and automated approaches such as the “Magecart” style digital skimming technique, in which malicious scripts infiltrate your e-commerce front-end and steal card data directly from users as they type it.

As a response to this threat environment, the PCI Security Standards Council has issued version 4.0 of PCI-DSS standards. The introduction of v4.0 represents a significant change from “point-in-time” compliance mentality to “continuous” security philosophy.

PCI-DSS 4.0 has been built around the concept of zero-trust architecture, MFA compliance requirements, and comprehensive engineering controls that will ensure the continuous operation and validation of your security controls.

2. Who Has to Be Compliant? The Four Merchant Levels

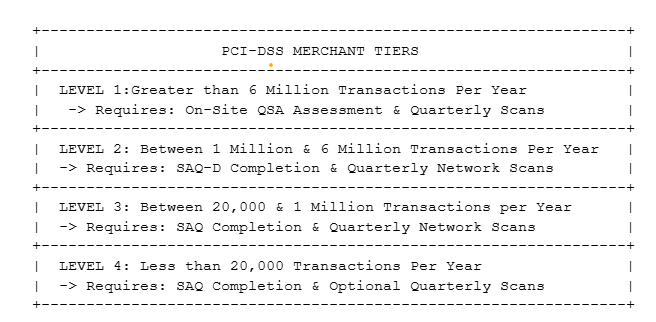

It is well understood by the payment card industry that there will be a massive difference between a micro-business with a couple of hundred transactions a year compared to a global marketplace that processes millions of transactions per day. For that reason, the industry has defined four tiers of compliance based on the total number of transactions within a rolling 12 month period.

Decoupling the Tiers

• Level 1: This level is allocated to large corporations that have transactions exceeding 6 million annually. Level 1 merchants will undergo strict assessment, requiring them to undergo an annual site assessment that is performed by a separate Qualified Security Assessor (QSA). The QSA will present a report called the Report on Compliance (ROC) along with required quarterly network scans externally.

• Level 2: These are merchants whose number of transactions falls between 1 million and 6 million annually. These merchants undergo a comprehensive annual Self-Assessment Questionnaire (generally SAQ-D), along with quarterly scans from outside parties.

• Level 3: This level includes those merchants that handle 20,000 to 1 million annual online transactions. These merchants perform a custom SAQ on a yearly basis, together with quarterly network vulnerability scanning.

• Level 4: These are merchants who conduct less than 20,000 annual transactions. They enjoy easy SAQ requirements every year but are fundamentally subjected to security policies.

Outsourcing Myth

One of the very risky myths that many e-commerce entrepreneurs hold is, “Since we outsource our checkout process using Shopify, Stripe, or PayPal, we do not need to concern ourselves with PCI compliance.”

This is totally incorrect. The simple fact is that while outsourcing your payment gateway takes some burden off (changing your audit from multiple pages to just a SAQ A or SAQ A-EP questionnaire), you are still responsible for everything else.

You are entirely responsible for making sure that the web page where your payment form appears has no viruses on it, that your login credentials are secure, and that your redirects are safe against being manipulated by any attackers.

3. The 12 Core Requirements of PCI-DSS Compliance

The design of PCI-DSS framework consists of six broad security objectives, each of which includes 12 core requirements. Let us unravel what these requirements mean in practice, presenting their equivalents in engineering terms.

Broad Objective A: Design and Operate Secure Network and Systems

Perimeter security of your IT infrastructure should provide full protection from any outside breaches.

- Requirement 1: Implement and Maintain Network Security Controls. This means creating a digital “moat” around your servers. The requirement implies deployment and configuration of firewalls, routers, and VPCs capable of examining all inbound and outbound traffic, effectively preventing any penetration into your environment where you process payments.

- Requirement 2: Implement Secure Configurations for All System Components. Manufacturers and developers always include default settings in their products, which could be something like a username as “admin” and password as “password123”. This requirement states that you must change the defaults, discontinue protocols that are not necessary, and make sure that every single server is hardened against any threat before connecting it to the network.

Overall Requirement B: Safeguarding Cardholder Data

This is the ultimate goal of PCI DSS compliance requirements. If you handle sensitive data in the form of finances, you must secure it with solid cryptographic methods.

- Requirement 3: Protect Stored Account Data. There is an axiom regarding data storage: if you do not require it, never collect it. When your system requires PAN data, such information must be stored securely either through encryption, truncation, or tokenization processes. Also, you should ensure that no SAD data is stored after authorization.

- Requirement 4: Use Strong Cryptography for Protection of Cardholder Data during Transmission. The process of transmitting data between the consumer’s mobile device/desktop browser to your store’s cloud server via public networks is extremely vulnerable to security breaches. In this regard, this particular requirement mandates that all cardholder data should be transferred using strong cryptographic methods such as Transport Layer Security.

Goal C: Conducting a Vulnerability Management Program

It’s difficult to achieve absolute security when it comes to software. What is perfectly secure on one day may not remain the same within days due to new vulnerabilities being discovered.

- Requirement 5: Ensure Protection of Systems and Networks from Malicious Software. Requirement 5 necessitates the implementation of an active and reliable anti-malware/anti-virus software that automatically updates itself and logs any malicious activity to eliminate threats like ransomware, Trojan, and spyware.

- Requirement 6: Build and Safeguard Systems and Software Security. The requirement entails the use of Secure Software Development Lifecycle (SDLC). Your developers must build their programs utilizing methods that ensure the programs resist exploitation through attacks such as SQL injection (SQLi) and Cross-Site scripting (XSS). Third-party systems, kernel-level operating system services, and program plugins must receive regular updates on the latest security patches.

D: Implement Stringent Access Control Practices

The more people that have access to your information system, the greater likelihood that there will occur insider incidents or credential thefts within the organization.

- Requirement 7: Basically, you should limit access to system components based on what is necessary for the completion of business operations. Permissions of access need to be highly restricted and stringent. There will be no need for frontend developers, digital marketers, and customer service representatives to see the actual databases containing payment transactions, because it will not serve any purpose for them to fulfill their respective roles within the organization. Access needs to be based on the principle of least privilege.

- Requirement 8: Identify Users and Control Access to System Components. Generic IDs or IDs created just for groups (e.g., dev_team and support_admin) are forbidden according to PCI-DSS requirements. All persons having access to the system need to have unique credentials identifying them as an actual user accessing the system. Moreover, MFA (multiple factor authentication) is now required under PCI-DSS version 4.0.

- Requirement 9: Limit Physical Access to Cardholder Data. If you are operating an ecommerce website using physical servers stored within an on-premise data center, then they need to have security features like access logs via keycards, biometric readers, and video cameras to protect against any sort of physical access.

Overarching Goal E: Constant Monitoring and Testing of Networks

You cannot protect yourself from an attack if you know nothing about what is taking place on your systems.

Requirement 10: System Component Access and Activity and Cardholder Data Access Must Be Logged and Monitored. When dealing with the aftermath of an incident, the most effective asset available to the forensic analyst is an intact audit trail. Under this pillar, it is expected that your systems will be logging all changes, activities, and accesses related to system components and cardholder data. The logs should then be collected in a central database, which is not accessible for alteration or wiping by any attackers.

- Requirement 11: Periodic Testing of Network Vulnerabilities. E-commerce environments are intricate networks comprised of constantly changing components. In compliance with this pillar, quarterly internal and external vulnerability scans must be carried out on your systems and networks, as well as regular penetration testing, when ethical hackers try to penetrate your systems in order to find vulnerabilities.

Overall Goal F: Uphold an Information Security Policy

No technology can ever be truly effective without a supportive organizational culture and process.

- Requirement 12: Underpinning Information Security Through Organizational Policy and Programs. Every organization should create and publish a complete information security policy. Such official documentation will become a blueprint of sorts for your entire company, detailing employee obligations, official procedures for handling data, obligatory security awareness training, and a well-thought-out incident response plan that can be successfully carried out in case of unforeseen trouble.

4. Understanding the Complex World of Data Security: Partnering for Compliance

It may not be easy for even the brightest engineers to get their heads around such a complex set of technological requirements as PCI-DSS while simultaneously expanding their online presence. Effective data protection entails a highly specialized expertise in network architecture, cryptography, cloud management, and audits.

In terms of many retail businesses scaling up, the effort to construct such sophisticated security pipelines themselves may end up being wasteful efforts that shift attention away from gaining customers and building products from the engineering team. It becomes much easier to achieve this by working together with cybersecurity firms offering dedicated cloud-based architecture software solutions.

Constructing a Managed Path to Compliance

A proper plan for achieving compliance usually revolves around four major strategic foundations for long-term security.

Gap Assessments: Security professionals perform comprehensive technical analysis of your existing architecture, management processes, and code deployments to directly compare the capabilities of your system to those required by the requirements of PCI-DSS v4.0. This way, any gaps, unencrypted data stores, and access flaws become apparent prior to audits by third parties or any other threats.

- Automated Evidence Collection for Audits: The old-fashioned way of preparing audits requires hundreds of hours of manual developer time spent logging, screenshotting, and confirming file configurations. In contrast, the new method involves installing continuous compliance software that connects directly to cloud providers via API endpoints, thereby creating continuous compliance verification trails to assemble the technical evidence needed to complete your yearly SAQ or QSA examinations.

- Scope Minimization: The best way to protect payment card information is not to have it within your business systems at all. With the help of security experts, you can learn how to segment and tokenize sensitive information so that your CDE is entirely isolated from the rest of your Web infrastructure. You can therefore reduce the scope of your CDE by 70%.

- Threat Monitoring: Data protection entails consistent monitoring for any possible threats. Through collaboration with a security firm, you get round-the-clock Threat Detection and Response services. Machine learning algorithms consistently scan through system log files, cloud activity, and network conditions in order to detect, control and resolve any anomalies well before they develop into data breaches.

5. Conclusion: Compliance is not just a Goal but a Process

When it comes to PCI-DSS compliance, one thing is clear – it is neither a one-off annual task nor a formality that can simply be fulfilled through the least effort. It is an ongoing and systematic commitment towards your customers’ interests. It is the way you assure them that you understand the value of their financial data and strive to protect it.

With the increasing sophistication and automation of cyber threats today, an effective security architecture is a crucial business differentiator in the online market environment. Combining the basic PCI guidelines with proper security architecture ensures that you successfully move your enterprise beyond the limits of reactionary response into a fully automated security mechanism.

Moving from a legacy solution-based software approach to a secure infrastructure requires highly technical know-how, and this is where the complete solution provided by Runtime Solutions can really help brands bridge the digital divide successfully. Launched in 2010, headquartered out of Mumbai, and quickly expanding its global presence across Kolkata, Nagpur, and Dubai, Runtime Solutions have been disrupting conventional digital practices for almost 16 years now. They function as a complete technology platform and a premium collaboration solution for digital transformations, catering specifically to organizations aspiring to grow within safe infrastructural parameters.

Using their expertise in product development and innovation consultants, organizations can implement elastic back-end commerce solutions that work efficiently with global payment standard registers. If you want to find out how to immediately transform your current retail infrastructure into one that harnesses the full-scale possibilities of secure digital commerce, you should explore the digital solutions provided by Runtime Solutions via the official Runtime Solutions Official Platform, which includes the entire list of services from their service catalog (Runtime Solutions Service Catalog).